Distribution Coverage—Why It’s Important to Understand the Difference Between MFFO and Cash

At Blue Vault, we report the sources of distributions in the Nontraded REIT Industry Review because we think it’s important to distinguish that Modified Funds from Operations (MFFO) is not the same as the Cash Available for Distributions. Even when MFFO “covers” the distribution amount, the actual cash needed to pay investors—or portions of it—might still be obtained from other sources such as offering proceeds or debt financing. But how can that be?

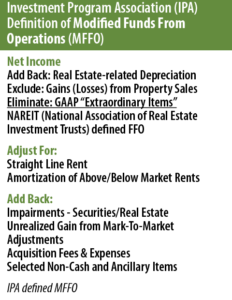

Defining MFFO

MFFO is not an alternative to cash flow, is not a measure of liquidity, and should never be considered in isolation or as a substitute for cash available for distributions.

MFFO is a supplemental measure of operating performance. MFFO is FFO (Funds From Operations) further adjusted to eliminate the impact of certain items that a nontraded REIT does not consider to be indicative of its ongoing operating performance.

The purpose of MFFO is to help investors in comparing performance across reporting periods on a consistent basis. It can be a useful tool to evaluate the effectiveness of the nontraded REIT’s business strategies and serve as a gauge for management performance.

Acquisition Fees & Expenses are real cash outlays. Many items in the FFO/MFFO calculation are non-cash charges on the income statement that do not, in fact, relate to an actual cash payment. Depreciation is the classic example.

But acquisition fees and expenses are real dollars paid out. Adding that amount back to compute an MFFO figure does not mean that the money is still available in the REIT’s cash coffers. It’s really gone. The acquisition fees and expenses amount cannot be applied toward paying actual distributions.

MFFO Doesn’t Account For Capital Expenditures

An important item missing in MFFO: the maintenance (or recurring) capital expenditures required to keep buildings in good working order. These include light fixtures, flooring repairs, paint, and general repairs. Those dollars are paid out in real life, but they are not subtracted from MFFO math. So MFFO would be reduced/lowered if capital expenditures were counted.

A Simplified Example

Of course, FFO and MFFO are not applicable to residential real estate. But for simplicity’s sake, let’s apply these nontraded commercial REIT metrics to your hypothetical foray as a first-time residential landlord:

- You buy your first rental house

- Your closing costs (i.e., acquisition costs) were $3,000

- Your rent the property for $18,000 annually

- Annual property taxes & insurance expenses are $5,000

- Annual depreciation on your rental property is $4,000

- You spend $2,000 improving the property

What would your “Personal MFFO” be versus available cash?

Let’s start with your Net Income:

Rental income = $18,000

– Depreciation on your rental property = $4,000

– Closing costs (i.e., acquisition costs) = $3,000

– Real Estate Property Taxes & Insurance Expense = $5,000

Net Income = $6,000

But the Depreciation expense IS NOT an actual cash outlay for you. So your “Personal FFO” and “Personal MFFO” would be:

Net Income = $6,000

+Depreciation on your rental property = $4,000

“Personal FFO” = $10,000

+Closing costs on your investment property purchase = $3,000

“Personal MFFO” = $13,000

So your “Personal MFFO” is $13,000. But do you really have $13,000 in cash? No. The $3,000 in closing costs were a real cash outlay for you. You don’t get that money back into your checking account. It was only added back to your “Personal MFFO” to make your results more comparable to those years when you aren’t buying new rental properties and to other landlords who aren’t actively buying properties.

And since the $4,000 depreciation was NOT a cash payment, that leaves you with $10,000 cash. But truthfully, you don’t have $10,000, either. Here’s why: You spent $2,000 improving the property. So your net cash is really $8,000. Paying out 100% of your “Personal MFFO” of $13,000 would leave you with a cash shortfall of $5,000 — that would have to be sourced from elsewhere.

Besides, you probably wouldn’t want to pay out the entire $8,000 cash, anyway. You might want to retain some of it for future purposes or put some of it toward paying down the mortgage loan on the property — that is, if you used financing.

Defining Cash (or Funds) Available for Distribution

Cash Flows From Operations can be helpful when considered in conjunction with MFFO. But since Cash Flows From Operations do not include recurring capital expenditures, it still doesn’t get investors all the information they need to calculate cash profitability.

As we look outside of nontraded REITs for best practices, we note that publicly traded REITs use a metric known as Cash (or Funds) Available for Distributions or AFFO (adjusted funds from operations) . This metric and it’s reconciliation to FFO is reported in quarterly supplements and usually includes the deduction of recurring capital expenditures, straight-lining of rents, as well as nonrecurring expenditures from their FFO calculations. As of yet, neither Cash (or Funds) Available for Distributions is a standardized figure because many publicly traded REITs define them differently. Nevertheless, adopting this type of practice may be another way for the nontraded REIT industry to more clearly articulate its source of distributions.