Blue Vault was founded on the belief that financial professionals need data and analysis based on fact, not opinion. For the past five years we have developed analytical tools and financial models that offer our clients the full picture of performance free of subjectivity and personal opinion. From our perspective, a truly effective performance measurement system should be based on multiple metrics using verifiable data and not limited to one-word labels or a simple color code.

With the introduction of our new Performance Profile System, we are continuing to enhance the transparency of nontraded REIT performance by leveraging the best practices of financial analysis. By adapting proven financial models used by public company analysts to nontraded REITs, we have taken our financial reporting to the next level by adding multiple layers within our measurement system that focuses on three essential areas; Operating Performance, Refinancing Outlook, and Cumulative MFFO Payout.

At the most basic level, here is a concise explanation of how we are doing it and what it means to you:

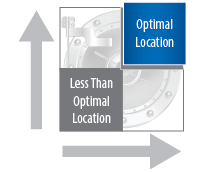

Using a four-quadrant performance profile system, we showcase the essential areas of

Using a four-quadrant performance profile system, we showcase the essential areas of

operating performance, refinancing outlook, and cumulative MFFO payout. Like many quadrant diagrams, the preferred location is the upper-right corner, while the less-than-optimal location is the lower-left corner.

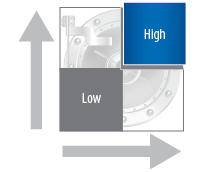

1. Operating Performance

This dimension examines the operations of a REIT based on the Leverage Contribution and Return on Assets. To provide shareholders with retu rns on a risk-adjusted basis, the REIT’s return on assets, which we measure as the latest 12-month MFFO as a percentage of the REIT’s assets, should exceed the yields available on 10-year Treasuries. In addition, when adjusted for the REIT’s use of debt, this return should exceed the REIT’s cost of debt, which indicates that leverage is effectively adding to shareholder returns. When the upper-right quadrant is highlighted, the REIT has managed its assets to provide a positive risk premium and has been effective in using debt to magnify returns to shareholders. Over time, any portfolio that includes debt financing should meet and exceed these two criteria.

rns on a risk-adjusted basis, the REIT’s return on assets, which we measure as the latest 12-month MFFO as a percentage of the REIT’s assets, should exceed the yields available on 10-year Treasuries. In addition, when adjusted for the REIT’s use of debt, this return should exceed the REIT’s cost of debt, which indicates that leverage is effectively adding to shareholder returns. When the upper-right quadrant is highlighted, the REIT has managed its assets to provide a positive risk premium and has been effective in using debt to magnify returns to shareholders. Over time, any portfolio that includes debt financing should meet and exceed these two criteria.

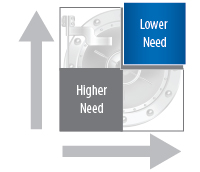

2. Financing Outlook

The purpose of this metric is to illustrate Interest Coverage Ratios and Refinancing Needs for each REIT. These two factors taken together will display the likelihood of a REIT’s need for refinancing in the near future and its ability to meet debt obligations.  The optimal placement for this dimension would be the upper-right quadrant, where there is a “lower need” to refinance because there is an Interest Coverage Ratio greater than the standard benchmark of 2.0x and less than 20% of its debt maturing within two years or at variable interest rates. Conversely, a REIT that has more than 20% of its debt maturing within two years or at variable rates and an Interest Coverage Ratio below 2.0x can improve its Financing Outlook by refinancing its short-term financing to longer maturity debt, converting variable-rate debt to fixed-rate, or improving its interest coverage by boosting income or lowering its cost of debt.

The optimal placement for this dimension would be the upper-right quadrant, where there is a “lower need” to refinance because there is an Interest Coverage Ratio greater than the standard benchmark of 2.0x and less than 20% of its debt maturing within two years or at variable interest rates. Conversely, a REIT that has more than 20% of its debt maturing within two years or at variable rates and an Interest Coverage Ratio below 2.0x can improve its Financing Outlook by refinancing its short-term financing to longer maturity debt, converting variable-rate debt to fixed-rate, or improving its interest coverage by boosting income or lowering its cost of debt.

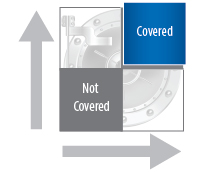

3. Cumulative MFFO Payout

The Cumulative MFFO Payout dimension gives an overview of the REIT’s cash distributions versus MFFO since inception, as well as the trend over the latest 12  months. This analysis highlights the REIT’s ability to cover its cash distribution payout to shareholders over time and indicates whether the trend is toward improved coverage. The optimal location is the top-right corner, which shows that a REIT has been able to fully cover its cash distributions on a cumulative basis and over the most recent 12-month period.

months. This analysis highlights the REIT’s ability to cover its cash distribution payout to shareholders over time and indicates whether the trend is toward improved coverage. The optimal location is the top-right corner, which shows that a REIT has been able to fully cover its cash distributions on a cumulative basis and over the most recent 12-month period.