How Rising Interest Rates Affect NTR Variable Rate Debt

October 21, 2022 | James Sprow | Blue Vault

Much of the variable rate debt used by nontraded REITs is tied to SOFR, the Secured Overnight Financing Rate that has replaced LIBOR as the floating rate benchmark for many debt instruments utilized by nontraded REITs to finance their acquisitions. For example, Blackstone Real Estate Income Trust (BREIT) has some variable rate borrowings whose rates are tied to SOFR. As of June 30, 2022, BREIT reported $29.8 billion in variable rate loans with weighted average interest rates of L+2.1 where “L” refers to the relevant floating rate benchmark which may include one-month LIBOR, three-month LIBOR, 30-day SOFR and one-month CDOR (a Canadian dollar-based index) as applicable to each loan.

As of December 31, 2021, the ICE Benchmark Association (“IBA”), ceased publication of all non-USD LIBOR and the one-week and two-month USD LIBOR and, as previously announced, intends to cease publication of remaining U.S. dollar LIBOR settings immediately after June 30, 2023. Further, on March 15, 2022, the Consolidated Appropriations Act of 2022, which includes the Adjustable Interest Rate (LIBOR) Act, was signed into law in the U.S. This legislation establishes a uniform benchmark replacement process for financial contracts maturing after June 30, 2023, that do not contain clearly defined or practicable fallback provisions.

The U.S. Federal Reserve, in conjunction with the Alternative Reference Rates Committee, a steering committee composed of large U.S. financial institutions, has identified the Secured Overnight Financing Rate (“SOFR”) a new index calculated using short-term repurchase agreements backed by U.S. Treasury securities, as its preferred alternative rate for USD LIBOR.

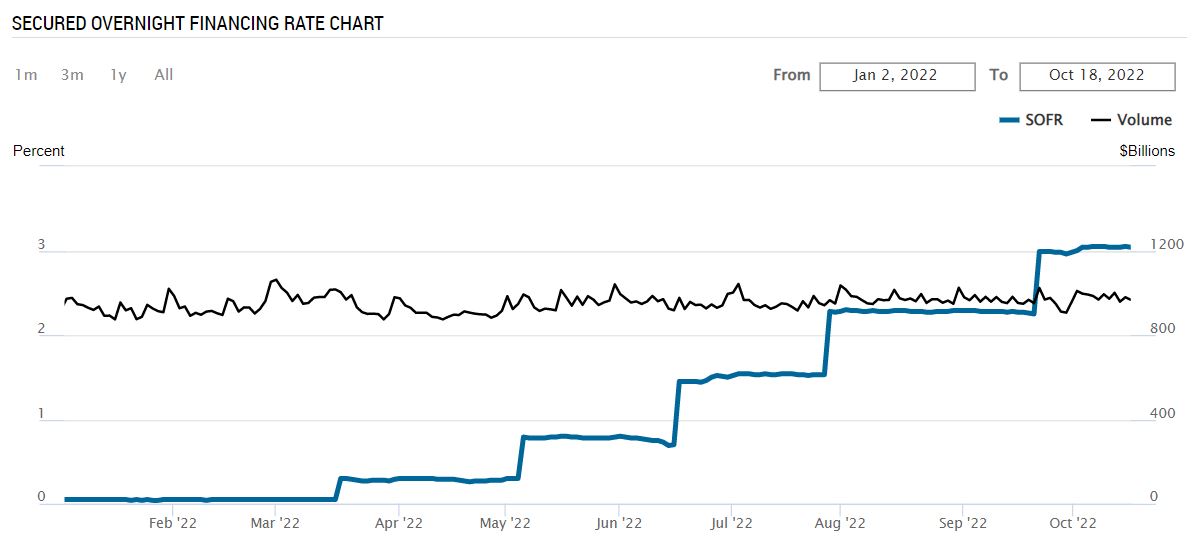

Since June 30, 2022, the one-month SOFR rate has increased from 1.69% to 3.04% as of October 18. This increase will impact the variable rates on NTR debt. Nontraded REITs utilize interest rate swaps to hedge the interest rates on their variable rate debt. BREIT reported on June 30, 2022, that it had swaps in place with an aggregate notional balance of $22.2 billion that mitigate the exposure to future interest rate increases on their floating rate debt.

Swap contracts are arrangements between the debtor and a counterparty, often a bank, to exchange the interest payment obligations on variable rate debt contracts for a fixed rate of interest. Simply put, the counterparty agrees to pay the variable rate of interest to the debtor and the debtor agrees to pay a fixed rate of interest to the counterparty. The result for the debtor is to convert what was previously a loan that had a variable interest rate for a fixed stream of interest payment obligations.

Blue Vault reports the fixed and variable rate debt of nontraded REITs, taking into consideration the hedging contracts like interest rate swaps. If a portion of a REIT’s variable rate debt has been effectively hedged via swap contracts, Blue Vault reports that debt as fixed rate debt.

Nontraded REITs also utilize contracts called “caps” to mitigate the effects of rising interest rates on their debt obligations when those debt obligations have variable rates of interest. An interest rate cap does not act as a hedge of interest rate risk until the rate on the variable rate debt reaches the cap rate. Once it exceeds the cap rate, the interest rate on the debt becomes fixed at the cap rate. In simple terms, caps are not “binding” until the variable rate reaches and exceeds the cap rate. Blue Vault reports the REIT’s variable rate debt which have caps as variable rate debt until the cap rate is reached.

For example, Blackstone REIT reported caps in place for 53 debt instruments as of June 30, 2022, with a notional value of $14.8 billion and a “strike” rate of 3.5%. They did not designate the caps as hedges on their variable rate debt, presumably because the index rates (LIBOR, SOFR or SIFMA) had not yet exceeded the cap strike rates. As index rates rise, these caps may begin to be effective hedges of the REIT’s interest rate risk. The weighted average maturity of the caps was reported as of June 30, 2022, as 1.1 years, indicating that the caps do expire over the next year.

As of June 30, 2022, Blackstone REIT reported an unrealized gain on their interest rate caps of $64.1 million for the first six months of 2022, meaning the caps the REIT had in place had already saved that amount in interest expense (roughly 9% of the REIT’s interest expense for the period).

Sources: SEC, Federal Reserve Bank of New York, Blue Vault