Relationships Between Cap Rates and Costs of Debt and the CRE Outlook

January 31, 2022 | James Sprow | Blue Vault

In commercial real estate, the concept of a “cap rate” or capitalization rate is a shorthand way of describing a property’s potential rate of return. A cap rate is computed based upon the net income a property is expected to generate divided by its asset value, expressed as a percentage. It is most useful in comparing the relative values of similar real estate investments.

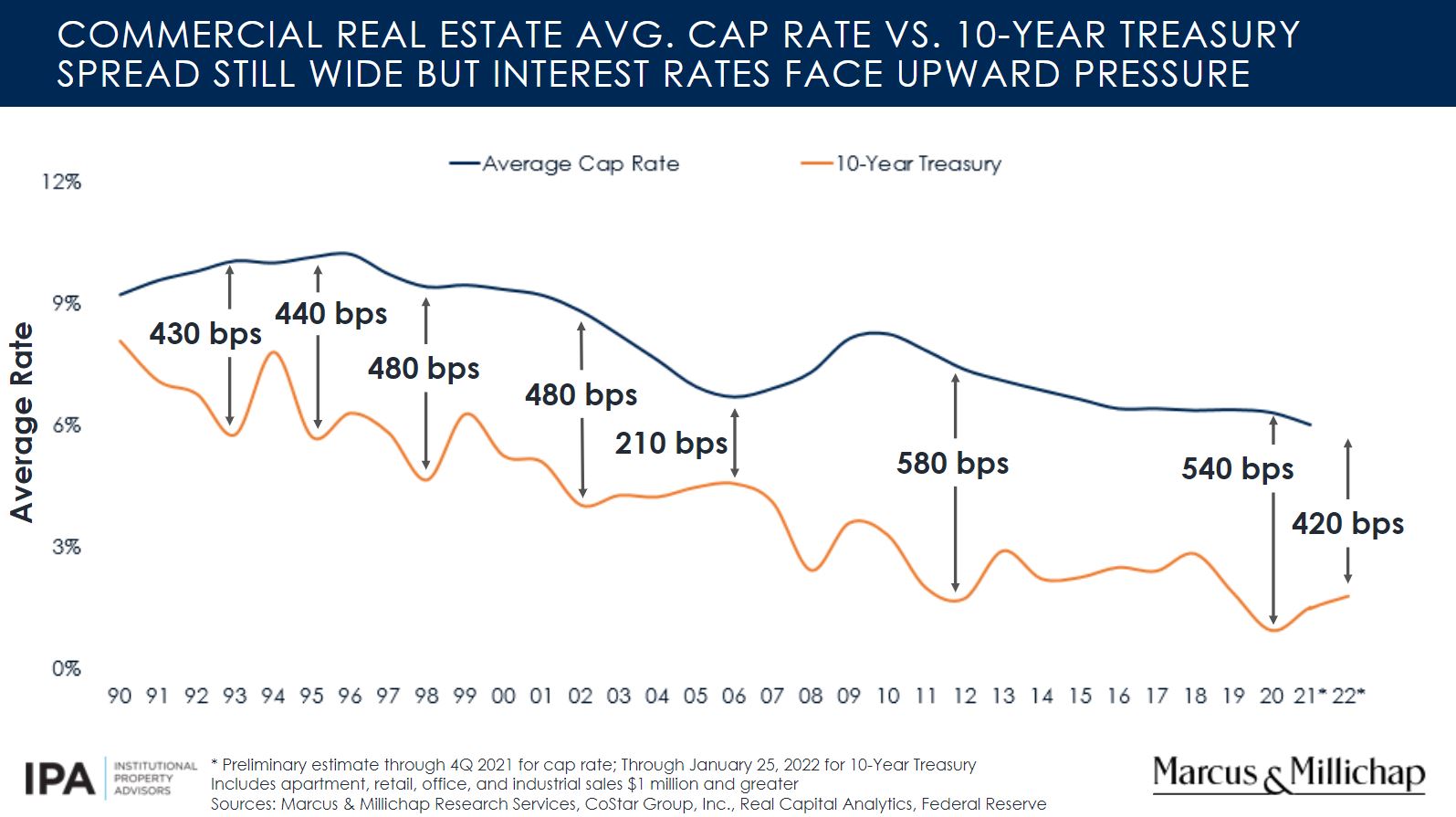

In a recent presentation by Marcus & Millichap, President and CEO Hessam Nadji showed a slide that compared the average cap rates for commercial real estate to the 10-year Treasury bond rate, going back to 1990. The spread between the two, expressed in basis points (“bps”) shows in simple terms the average expected return on commercial real estate investments versus a proxy for the cost of financing those investments. Other things equal, investors do better when that spread is greater, meaning they can earn relatively more on the real estate investment than the cost of borrowing.

We are currently in an environment when real estate investors are expecting borrowing rates to rise. The Fed has been signaling that the easy money regime that has been in place during the pandemic is going to end and concerns about inflation will be outweighing the need to support the economy by maintaining historically low interest rates. The recent uptick in borrowing rates can be seen in the 10-year Treasury rate in the slide below.

Cap rate compression, the lowering of average cap rates, has been the story over the past decade and has continued during the pandemic. When looking at the chart, the question naturally arises if cap rate compression can continue as borrowing rates rise. The spread between cap rates and 10-year Treasury rates reached a 540 bps level in 2020 but has since narrowed to a recent 420 bps rate mark.

One important factor to remember is that cap rates are based upon current net income levels and current property values. This means that investors can accept lower cap rates in their valuations if they expect net income to increase, other things equal. The expected rate of return on a commercial real estate investment isn’t determined just by the current ratio of income to value, but rather, by current income plus future growth in that income to current valuations. For example, if rents are expected to grow faster than expenses for a given property, then today’s low cap rate based upon near-term net income can be acceptable. Properties that have higher growth potential in rental rates will have lower cap rates, other things equal. Naturally, investors also consider the riskiness of those future net income projections and will demand higher cap rates (lower property prices) with riskier future cash flows.

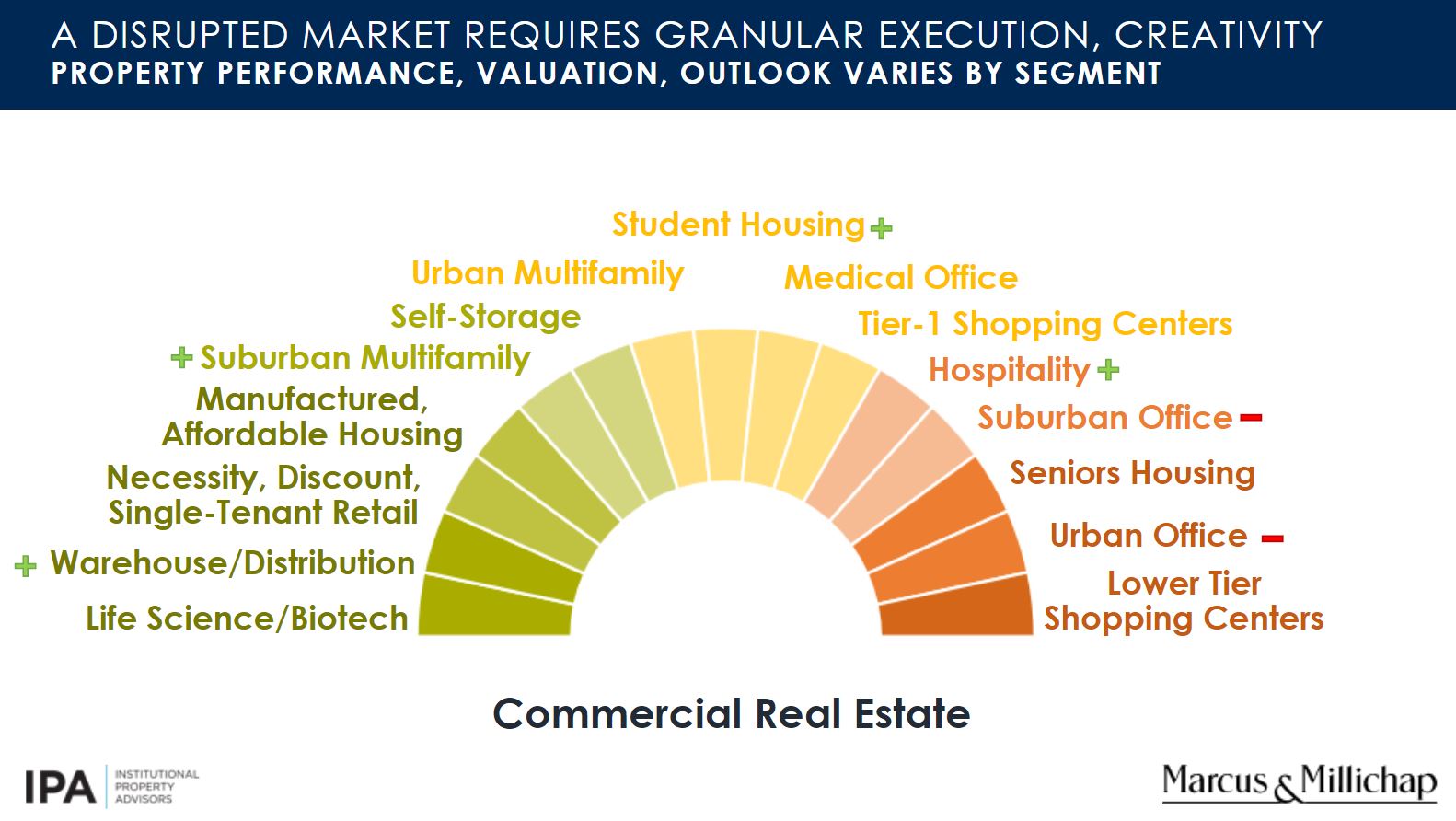

A second interesting slide that Marcus & Millichap included in their presentation is shown below. This slide emphasizes that today’s commercial real estate market has been disrupted greatly by the pandemic, and the impacts of the pandemic and the shocks to the economy it has created, have affected different commercial real estate sectors differently. As the economy recovers, different property types will have different trajectories in terms of performance in the months and years ahead.

Several of the strongest performing asset classes over the last two years have been warehouse/distribution, necessity retail, multifamily and self storage. Nadji expressed optimism about those top performers going forward. On the other end of the spectrum, lower-tier shopping centers, urban office, seniors housing and hospitality have been poor performers and may be slower to recover.

Investors in commercial real estate will be focused on both cap rates across the spectrum of asset types available, and the expected growth rates in rents. The supply constraints we are observing in warehouse/distribution assets have been leading to record occupancies and high growth rates in rents. Likewise, multifamily assets have seen strong rent growth and growing demand as rises in home mortgage rates and constrained production of single family homes, will continue to make multifamily assets more valuable. With short-term leases, multifamily property owners can respond to increasing demand by increasing rental rates.

The presentation on January 27 by Marcus & Millichap highlighted some of the important trends in cap rates, interest rates, and their impact upon the different sectors of the commercial real estate market.

Source: Marcus & Millichap