Blackstone REIT’s Use of Interest Rate Derivatives to Protect Against Interest Rate Increases

August 29, 2022 | James Sprow | Blue Vault

As of June 30, 2022, Blackstone REIT had $29.8 billion in variable rate loans secured by the Company’s real estate. The REIT also had $22.2 billion in the notional balance of its interest rate swap contracts that mitigate its exposure to potential future interest rate increases on its floating-rate debt. The weighted average interest rates on the variable rate debt range from L+1.7% to L+3.5% with a weighted average rate of L+2.1% where the “L” refers to the relevant floating rate benchmark rates, which include one-month LIBOR, three-month LIBOR, 30-day SOFR1, and one-month CDOR as applicable to each loan.

Another method the REIT utilizes to protect its liabilities from increasing interest rates is an interest rate cap. An interest rate cap sets an upward limit on the rate of interest that the REIT is obligated to pay on property debt contracts. As of June 30, 2022, the REIT had 53 cap instruments in place on $14.8 billion in notional amount of property debt. The caps have a strike (the rate to which the variable rate could rise before it would be fixed) of 3.5%2 according to the REIT’s 10-Q.

An interest rate swap is a forward contract in which one stream of future interest payments is exchanged for another based on a specified principal amount. Interest rate swaps usually involve the exchange of a fixed interest rate for a floating rate, or vice versa, to reduce or increase exposure to fluctuations in interest rates or to obtain a marginally lower interest rate than would have been possible without the swap. Swap contracts can be negotiated with banks that have other customers that are willing to accept floating rates in lieu of fixed rates on their outstanding contracts.

The notional principal amount in an interest rate swap, is the predetermined dollar amounts, or principal, on which the exchanged interest payments are based. Notional principal amounts are the theoretical value that each party pays interest to the other at specified intervals. With a swap contract, the principal is not paid, but is used only to calculate the relevant interest payments to be exchanged.

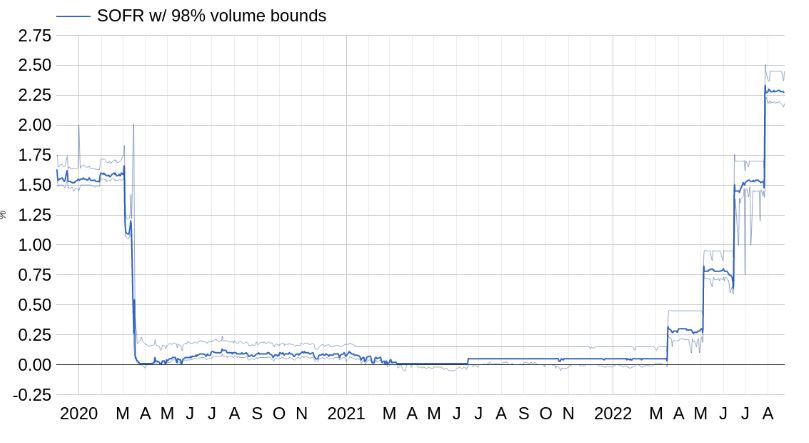

With swap contracts indexed to SOFR, LIBOR or EURIBOR, Blackstone REIT states in its 10-Q as of June 30, 2022, that the total notional amount of its 38 swap contracts of $22.2 billion has a “strike” of 1.9% and a weighted average maturity of 8.1 years. In the chart below, we see that the regime of rising interest rates in the U.S. has resulted in a dramatic increase in the SOFR index. Between June 2022 and August 2022, the SOFR index has risen from 0.75% to over 2.25%, above the 1.9% “strike” that is stated in the REIT’s 10-Q. This rise in rates indicates that BREIT is probably benefiting from the swap contracts it has in place.

For the first six months of 2022, the REIT had interest expense of $722.2 million and increased its property-related borrowings during that period from $61.1 billion to $74.0 billion. For the first six months of 2022 the REIT had a net loss of $714.5 million. If the interest rate swaps and caps in place as of June 30, 2022, effectively limit the interest expense posted by the REIT going forward, they will have a meaningful impact on the REIT’s net income or loss, given the relative proportionality of the interest expense and the net loss recorded in the first half of 2022.

Footnotes

1. The Secured Overnight Financing Rate (SOFR) is intended to replace the US dollar London Interbank Rate (US LIBOR) in future financial contracts. SOFR was selected by the Alternative Reference Rates Committee (ARRC) chaired by the New York Federal Reserve in 2017.

SOFR is the average rate at which institutions can borrow US dollars overnight while posting US Treasury bonds as collateral. Similar to a mortgage rate, SOFR is a secured borrowing rate in the sense that collateral is provided in order to borrow cash. SOFR differs from US LIBOR in that the latter is a rate for unsecured borrowing (where no collateral is posted).

2. The 3.5% strike for the 53 cap instruments with a notional amount of $14.8 billion may represent a weighted average cap rate. It is stated on page 31 of the Q2 2022 10-Q.

Sources: SEC, Investopedia, www.sofrrate.com