James Sprow | Blue Vault |

In today’s turbulent financial markets it’s very difficult to identify safe havens for investment. With regard to commercial real estate, two measures of relative safety might be the combination of a real estate portfolio’s weighted average occupancy and its weighted average lease maturity. In simple terms, the higher the occupancy level and the longer the average lease terms the better. Of course, the quality of tenants is important as well, as are the types of tenants. The credit-worthiness of the corporations that lease properties is a very important consideration and many REITs are justifiably proud of their high percentage of financially strong tenants. Also, nontraded REIT managers extol the virtues of “necessity-based retail” and “triple-net leases” as qualities that tend to insulate their cash flow streams from the ups and downs of the economy. Necessity-based retail usually includes grocery-anchored shopping centers, pharmacies, discount stores, and service establishments. These types of tenants tend to be relatively more immune to the ups and downs of economic cycles. They also tend to be more immune to the rapid growth of online shopping. Triple-net leases protect the property owners from the responsibilities for maintenance, taxes, insurance, and other expenses that are borne by the tenants and their corporate owners.

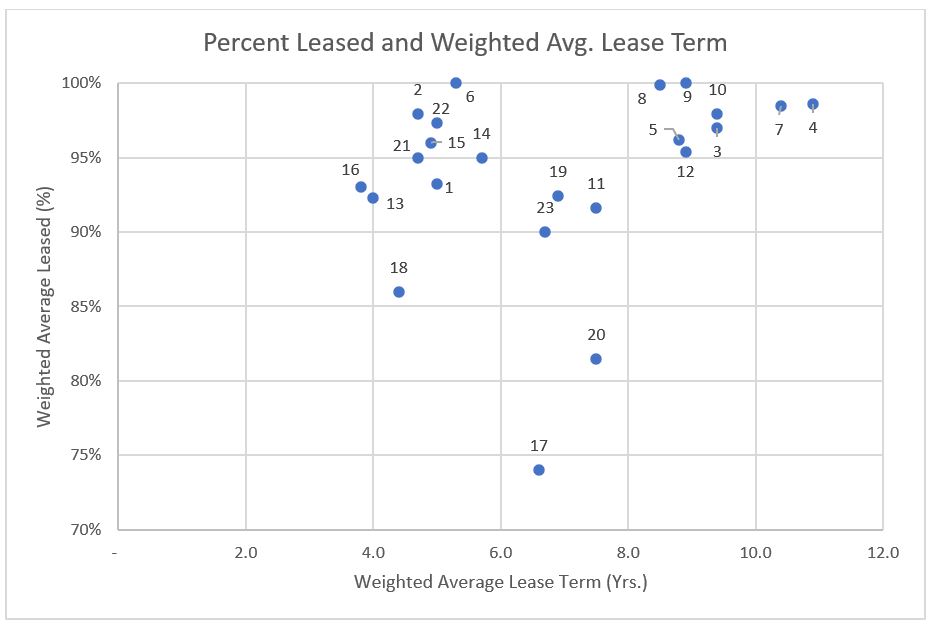

Looking at the combination of occupancy rates and lease maturities for the nontraded REITs in the Q3 2019 Blue Vault Nontraded REIT Industry Review, we can identify those REITs that have two attractive metrics: high occupancy rates and longer-term leases. In the plot below, those REITs are found in the upper right area of the scatter plot.

As expected, the REITs with a good combination of high occupancies and long-term leases tend to be those with triple-net leased retail properties. And, as expected, a look at their tenant rosters will confirm that they tend to have leases with more necessity-based or recession-resistant tenant types.

REITs 4, 5, 7, 8 and 9 are all advised by CIM. The tenants in CIM Income NAV (4), CIM Real Estate Finance Trust (5) and Cole Credit Property Trust V (7) are predominantly triple-net leased, recession-resistant retail tenants. The two Cole Office & Industrial REITs (8 and 9) have high occupancy rates. Carter Validus Mission Critical REIT II’s tenants are in the healthcare and data center asset classes. Corporate Property Associates 18 – Global (10) is a well-diversified, maturing REIT.

On the other end of the spectrum, REITs like KBS REIT II (17), KBS REIT III (18), KBS Growth & Income REIT (16) and NorthStar Healthcare Income (20) are not doing so well, and two of them are in the process of liquidation. Industrial Property Trust (13) was sold to ProLogis in January 2020.

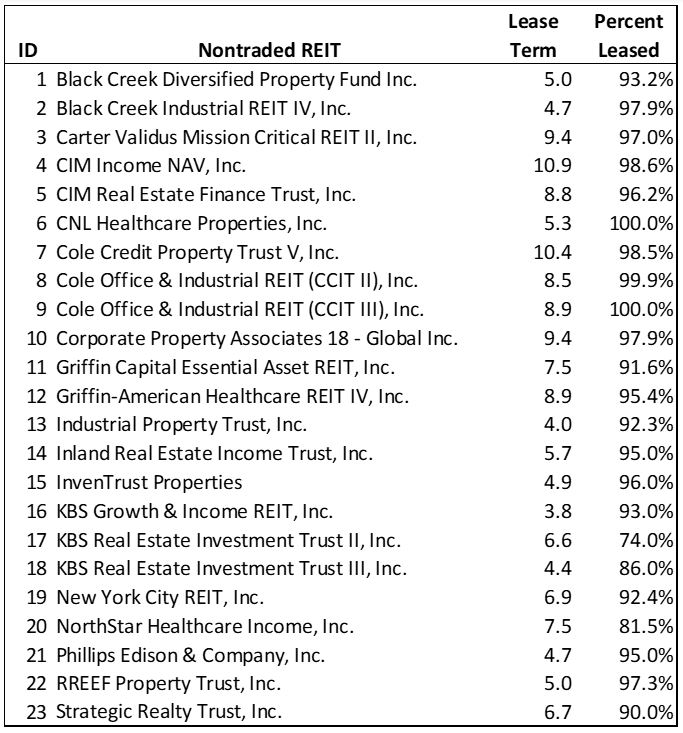

Legend (Lease Term and Percent Lease are weighted averages based upon GLA):