Johnathan Rickman | Blue Vault

According to Blue Vault data, the nontraded REIT industry continued to face challenges in the fourth quarter of last year, including with distribution coverage and acquiring assets. One bright spot, however, was a sharp increase in fundraising—an encouraging sign that comes amid a recent uptick in the introduction of Delaware Statutory Trust (DST) programs.

Let’s take a closer look at the data, based on findings from Blue Vault’s Q4 2025 Nontraded REIT Industry Review and new, searchable research portal.

Capital Raise

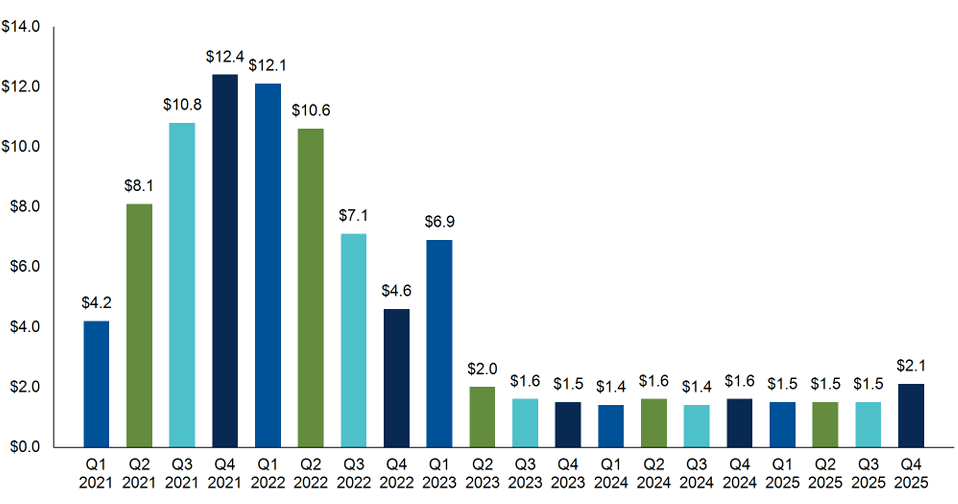

The nontraded REIT industry raised approximately $2.13 billion in public funds in the fourth quarter of 2025, the highest quarterly total since Q1 2023, and up from the $1.46 billion raised in the third quarter of last year.

Nontraded REIT Capital Raise in $ Billions (Quarterly, through December 31, 2025)

The industry’s quarterly capital raise had hovered between approximately $1.4 billion and $1.6 billion over the prior nine quarters before eclipsing the $2.0 billion mark in Q4 2025.

In addition to the public capital raise, the funds included in Blue Vault’s Q4 report raised approximately $2.72 billion through private offerings in the fourth quarter.

Blackstone Real Estate Income Trust has dominated the sector since it was introduced in 2016 and it led the way in Q4 2025, raising $1.4 billion in public offerings. That amounted to a 67.4% market share, having raised an estimated total of $84.7 billion since inception.

Other top capital raisers since inception and as of December 31, 2025, include Nuveen Global Cities REIT ($157.7 million), Hines Global Income Trust ($146.8 million), FS Credit REIT ($134.3 million), and Apollo Realty Income Solutions ($106.4 million).

More high-profile alternative investment firms are turning to the DST structure—some for the very first time—to raise capital. With giants such as Blackstone and even smaller firms such as Sealy & Company launching new DST platforms last year, the industry is, intentionally or not, reviving advisor interest in the sector.

Based on most recent filings and the offerings tracked by Blue Vault—including nontraded REITs and real estate-focused business development companies, interval funds, and tender offer funds—private real estate as an asset class raised $4.4 billion in Q4 2025.

Asset Levels

The industry’s assets under management have fallen over the last several years and recent results continued that trend. As of December 31, 2025, the industry had $169.4 billion in AUM, down from $174.1 billion in the third quarter of 2025, $178.0 billion in Q2 2025, and $184.3 billion in Q1 2025.

As to be expected, Blackstone REIT leads the sector in total assets, managing $98.6 billion as of December 31, 2025, making up 58.2% of the industry’s total. Starwood REIT once again came in second with $18.9 billion in reported assets, for 11.2% of the industry’s total. FS Credit REIT was once more the third-largest offering with assets totaling $11.8 billion.

The drop in industry AUM can be attributed to a combination of factors: less fundraising, rising redemptions that have forced asset selloffs, and funds liquidating or going public.

Based on most recent filings and the offerings tracked by Blue Vault—including nontraded REITs and real estate-focused business development companies, interval funds, and tender offer funds—private real estate as an asset class managed $236.6 billion in assets in Q4 2025.

Distributions

A consistent bright spot for the industry has been median distribution yields (Class A or Class T) for open REITs, which have held steady in the 5% range for the last four quarters—and rose in the fourth quarter:

| Reporting Period | Median Distribution Yield |

| Q1 2025 | 5.06% |

| Q2 2025 | 5.00% |

| Q3 2025 | 5.06% |

| Q4 2025 | 5.12% |

However, maintaining these yields has come at a cost, namely leverage. Median funds from operation (FFO) payout ratios for open REITs have been over 120% over the last five quarters, reaching as high as 177% in the fourth quarter of 2024.

| Q4 2025 Median | Q3 2025 Median | Q2 2025 Median | Q1 2025 Median | |

| Open REIT FFO Payout Ratio (YTD)* | 141% | 132% | 127% | 123% |

*Excluding REITs with “Not Meaningful” or “N/A”

The industry’s median debt ratios for open REITs rose in the fourth quarter as well, rising to 46% from 40% during the previous quarter.

Redemptions

Redemption gating has been an ongoing industry trend over the past several quarters, but a turnaround appears to be taking shape.

Blue Vault’s coverage of the nontraded REIT industry as of December 31, 2025, includes 25 active and open REITs. Of those, only three nontraded REITs gated redemption requests in the fourth quarter of 2025: Cantor Fitzgerald Income Trust, Inc., RREEF Property Trust, Inc., and Starwood Real Estate Income Trust, Inc.

For the quarter ending December 31, 2025, Blackstone REIT repurchased 85.8 million shares of common stock for a total of $1.2 billion, representing 2.4% of its net asset value. The nontraded REIT had no repurchase requests go unfulfilled in the fourth quarter of 2025.

Starwood REIT continues to receive repurchase requests that far exceed its monthly and quarterly limits. In each of the three months of the fourth quarter of 2025, the nontraded REIT fulfilled only 4% of repurchase requests. Starwood subsequently suspended its share repurchase program.

Don’t Go It Alone

Learn about Blue Vault membership and how our performance data can help protect your clients, and as such, your advisory practice. Our research includes historical and current data on nontraded REITs, nontraded BDCs, interval funds, tender offer funds, and preferred share stock. Our coverage also includes capital market overviews, financing outlooks, individual performance profiles, and updates on product launches and full-cycle events.

With the launch of Blue Vault’s new research portal, wealth advisors can sort, filter, and analyze private equity, credit, and real estate offerings like never before.

Are you an asset manager, broker-dealer, or other firm serving the alts industry? Contact us today to view a full demo of our unparalleled research offerings.