The Logic Behind Taking Listed REITs Private

April 26, 2022 | James Sprow | Blue Vault

The headline on April 25 stated that Blackstone Inc. (Ticker: BX) agreed to buy another real estate investment trust (REIT) PS Business Parks (Ticker: PSB) for $7.6 billion, including debt. The deal would take the REIT private and pay shareholders of PS Business Parks a 12% premium over the stock’s closing price on Friday, April 22. This is just the latest of Blackstone’s acquisitions of listed REITs. Last week it agreed to purchase American Campus Communities for $12.8 billion, a REIT that owns 166 properties across 71 university markets across the U.S. That deal would pay shareholders an estimated 14% premium over the REIT’s previous closing price.

Of course, the most famous example of an offer to take a listed company private is the deal put forward last month by Elon Musk to buy Twitter. He has offered shareholders a premium roughly 37% above the closing price prior to his announcement of $39.43. In his public statements, the motive is to promote free speech and making Twitter’s algorithms that determine what posts are “acceptable” more transparent. But it can’t be overlooked that, should his attempted purchase of Twitter be consummated, the platform could become more valuable and reward Musk and his backers with a financial profit as well as a victory for free speech.

In the interesting case of Blackstone’s spate of acquisitions of listed REITs, we can assume that there is no higher principle involved than buying assets that are, in the eyes of the beholder, undervalued. Presumably, Blackstone looks out at the world of listed REITs, of which there are over 300 according to NAREIT, and finds those that fit their plans for constructing real estate portfolios and which are also selling at bargain prices. How does Blackstone, or any other potential acquiror of a listed REIT, evaluate whether the REIT is selling at a bargain price? The easy answer to that question begins with a simple calculation: the ratio of price to NAV.

The net asset value of a listed REIT is simple to calculate. It is calculated by subtracting the fund’s liabilities from the total value of the REIT’s assets. One could argue that the fund’s share price actually represents the market’s estimate of its net asset value per share. But analysts may have a different estimate of a REIT’s net asset value per share if they believe that the market price of the fund’s shares does not accurately represent its “true” value. Simply put, if shareholders agreed that expert analysts were correct in valuing a REIT’s shares more highly than the market price, they would be willing to buy more shares, and if they believed the market analysts’ view that the market share price was higher than the REIT’s “true” net asset value per share, they would likely be net sellers of the shares. The analysts at Blackstone that recommended to the company’s management that its recent offers to take listed REITs private obviously believed that the “true” value of the REITs, at least to Blackstone, were above the market prices of the REITs’ shares.

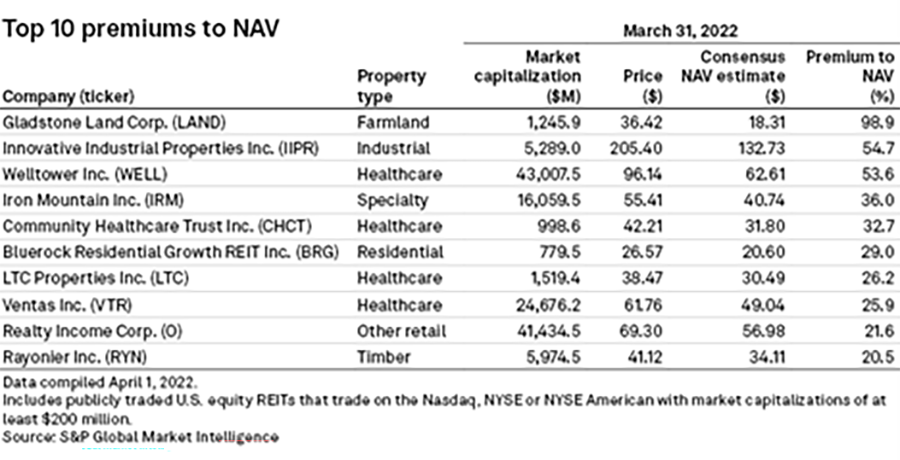

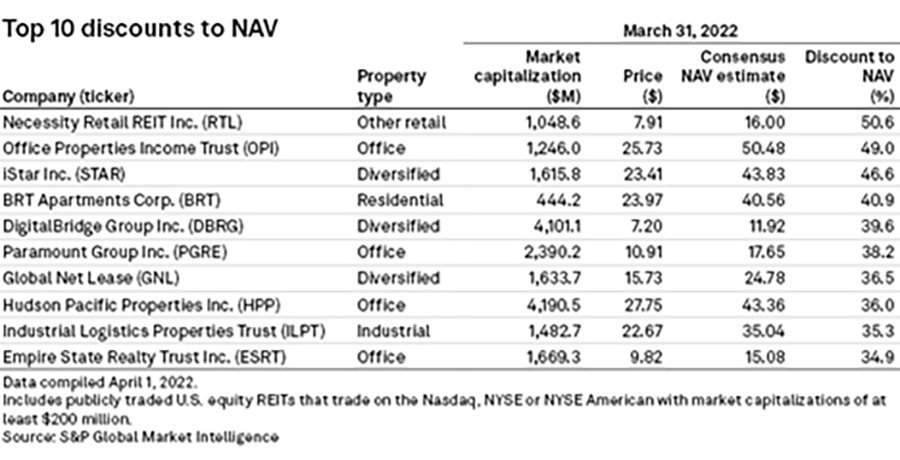

S&P Market Intelligence provides monthly a list of REITs that are trading above, at a premium, or below, at a discount, to their NAVs. The net asset values in these lists are estimated by the analysts covering the REITs, and the premium or discount to the estimated NAVs is calculated as the ratio of the most recent closing price of the REIT’s shares to the median estimated NAV by the analysts. The monthly reports list those REITs with the largest premiums to NAV and the largest discounts to NAV, as well as the median premiums and discounts to NAV for REITs grouped by property type.

In an April 5 report by S&P Market Intelligence, the top ten discounts to NAVs among the listed REITs ranged from discounts of 50.6% to 34.9%. The top ten premiums to NAVs among the listed REITs ranged from 98.9% down to 20.5%. This raises the question, “Why would analysts who study these listed REITs have such a different view of their real values than the market appears to have?” One answer to that question is that the analysts have better information than those shareholders who are buying and selling the REIT shares. Another perspective is that the logic behind determining a REIT’s NAV per share is different for shareholders than for analysts. To the extent that NAVs are estimated using historical or GAAP accounting numbers and market prices are determined using expectations of future cash flows, it might be expected that the two would differ. Indeed, it does not take much of a divergence between the estimates of analysts regarding the future growth prospects of a REIT’s cash flows from its historical trends to arrive at a significant difference in NAV estimates.

Looking at the S&P Market Intelligence article from April 5 that lists the top ten REITs with a premium to NAV, one recently announced Blackstone acquisition that will be closed soon is the offer to purchase Bluerock Residential Growth REIT (Ticker: BRG). The reports shows that REIT trading at a March 31, 2022, premium to NAV of 29%.

Blackstone announced the agreement to acquire Bluerock Residential Growth REIT on December 20, 2021, for $24.25 per share. Prior to the acquisition, BRG intends to spin off its single-family rental business to its shareholders, which could account for the difference between the March 31, 2022, price, and the offer by Blackstone. But it is to be noted that Blackstone offered a premium of 124% over the unaffected share prices on September 15, 2021, the day before an article appeared reporting that BRG was exploring strategic options, including a sale.

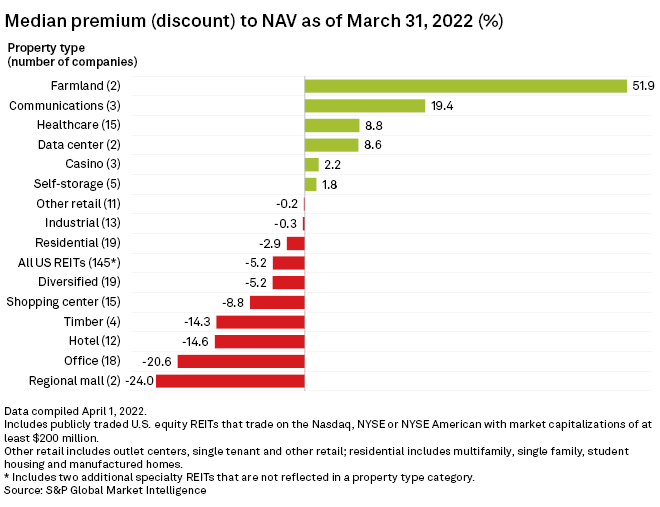

While the premium price reported for these ten listed REITs can be explained in the case of BRG, there is probably a unique story for each of the nine others. The next offer to take a listed REIT private may very well involve one of the REITs that the analysts believe is selling at a discount to net asset value. If not one of the REITs listed below, perhaps among the asset types that have a median discount to NAV, as shown in the chart below.

Sources: S&P Global Market Intelligence, Bluerock Residential Growth REIT, Blackstone