Digging Deeper into ARC New York REIT Expenses and Performance

June 19, 2018 | James Sprow | Blue Vault

On June 13, 2018, Blue Vault published an article exploring the performance of the nontraded REIT American Realty Capital New York REIT, Inc. In that article, we referenced the recent update of the REIT’s estimated NAV per share from the previous value of $21.25 to a new value as of June 30, 2017, to $20.25. We asked why NAV was dropping given that the REIT’s portfolio of six Manhattan properties had not changed since the June 30, 2016, date. The board of directors also suspended distributions effective March 1, 2018.

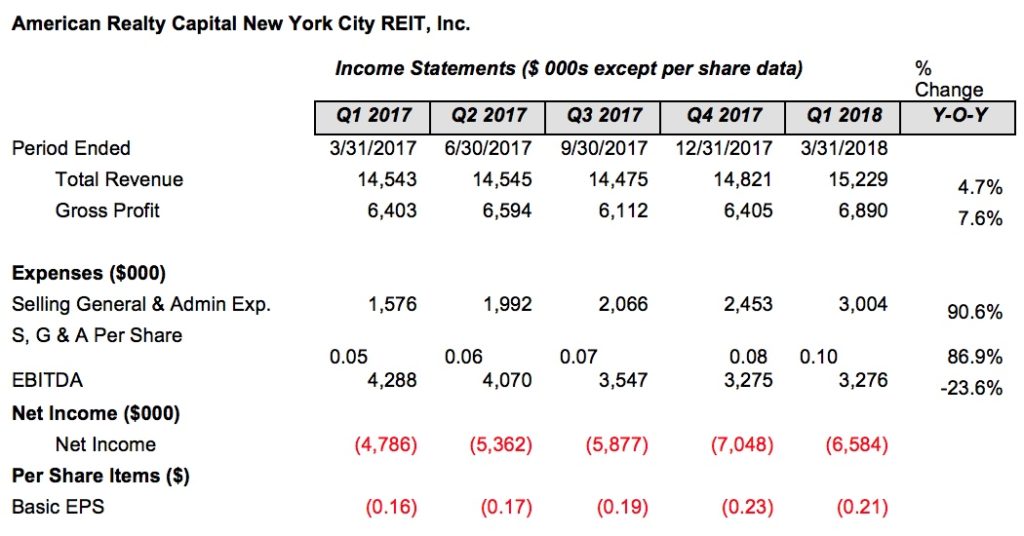

We highlighted the increase in REIT’s General and Administrative expenses over the past five quarters from $1.576 million in Q1 2017 to $3.004 million in Q1 2018. That increase represented a change from $0.05 per share in Q1 2017 to $0.10 per share in Q1 2018. Clearly, the increase in those expenses can impact the estimated NAV per share.

We also compared the occupancy rates at the time the properties were acquired to their respective occupancies on March 31, 2018. We illustrated that the occupancy rates for the three largest properties had all declined since their respective acquisitions. These declines in occupancy rates would also impact the NAVs per share. Compared to the increase in expenses, the increase in rental revenues over the last five quarters has not kept pace. The result has been a decline in net income from a loss of $4.786 million in Q1 2017 to a loss of $6.584 for Q1 2018.

In a call with Jon Trump at ARC New York REIT on June 15, we were directed to the REIT’s 10-K where the increase in expenses is addressed.

We found the following partial explanation in the 10-K:

General and Administrative Expenses

General and administrative expenses increased $1.4 million to $3.0 million for the three months ended March 31, 2018, compared to $1.6 million for the three months ended March 31, 2017, primarily related to an increase in general and administrative expense reimbursements incurred from our Advisor, as well as an increase in legal and proxy fees. General and administrative expense reimbursements incurred from our Advisor increased $0.5 million to $1.1 million for the three months ended March 31, 2018, compared to $0.6 million for the three months ended March 31, 2017. The legal and proxy fees contributed approximately $0.8 million to the increase in general and administrative expenses during the three months ended March 31, 2018 when compared to the three months ended March 31, 2017, which included approximately $0.4 million paid under an agreement entered into to settle the contested vote at our 2017 annual meeting of stockholders.

We estimate that the increase alone of $1.6 million in the year-to-year quarterly expenses amounted to approximately $0.05 per share:

$1.6 million/31,431,555 = $0.05 per share

And the total increase from Q1 2017 to Q1 2018 totaled about $0.10 per share.

Over the course of five quarters, we observe the following trends:

Since 2016, the REIT has filed numerous proxy statements with the SEC relating to amendments to the Company’s charter which have required shareholder approval. The REIT has also filed a self-tender offer in response to a third party tender offer. Without exploring each of these actions further, it is safe to conclude that a substantial portion of the increase in expenses has been due to increased legal fees related to proxy solicitations and tender offers, which was confirmed in our conversation with Jon Trump.

With regard to occupancies and rental revenues, we found the following in the 2017 10-K:

In order to meet our investment objectives, we have acquired and may continue to acquire assets that have less than 80% occupancy, but which we believe we can reposition, redevelop or remarket to create value enhancement and capital appreciation opportunistically. For example, we acquired 9 Times Square in November 2014 at 50.3%*occupancy and as of December 31, 2017, occupancy was at 63.9%. Subsequent to acquisition, we allowed leases to expire and terminate as part of the implementation of our repositioning, redeveloping and remarketing plan with respect to the property. While we have substantially completed our repositioning and redevelopment plan with respect to 9 Times Square and are currently working to lease the remaining vacant space at the property, there can be no assurance that we will be successful in lease-up of this property or effectively repositioning or remarketing any other property we may acquire for these purposes, including increasing the occupancy rate.

*The press release at the time of the acquisitions states that: “570 Seventh Avenue contains approximately 170,000 rentable square feet and is currently 76% leased as of the acquisition date.” It appears that the property was subsequently re-named or re-branded as “9 Times Square.”

Looking at the REIT’s capital expenditures which we assume have been made to increase the income potential for its three largest properties, we see that the REIT has reported over $27.6 million in capex since 2015. Altogether, these capital expenditures would amount to approximately $0.92 per share. It might be reasonable to expect capital expenditures made to improve the income potential of the REIT’s largest properties would begin to bear fruit and be reflected in the REIT’s income statements, or at the very least in its occupancy rates. The capital expenditures have dropped from a quarterly average of $4.2 million in 2016 to $2.7 million in 2017 to just $76,000 in Q1 2018. Again, assuming the capital improvements have been largely completed, we have yet to see them positively impact the REIT’s bottom line.

To summarize, ARC New York City REIT, Inc. has yet to capitalize on the actions the board has taken over the past two years to reposition itself for a future liquidity event. Its estimated NAV per share has dropped, along with its net income per share, and it recently eliminated cash distributions to its shareholders. Blue Vault concludes that shareholder value has been reduced and, based upon public information, the REIT’s goal of increasing the value of its portfolio of six Manhattan buildings has not yet succeeded.

Sources: SEC; conversation with Jon Trump on June 15, 2018; Blue Vault

Learn more about AR Global on the Blue Vault Sponsor Focus page

How to Explain ARC New York City REIT Performance?